The Expansion of Indian Steel: Companies are risking more than reputation

Jun 4, 2023

By Paul Griffin

As steel companies waste no time in deploying new blast furnaces in India, they not only lock themselves into a path of carbon dioxide and methane emissions, they lock themselves into a risky and inflexible business model.

Reaping the demographic dividend

India is the second largest steel producing country in the World1. With an annual production in 2022 of 115 million tonnes (Mt), India still produces eight times less crude steel than China, but the gap is set to narrow significantly over the coming decades.

The potential for growth in Indian steel is considerable. Now the most populous country on Earth2, and with a median age of just 283, India is poised to reap its demographic dividend. Simultaneously, apparent steel use (ASU) per capita in India is low: just 80 kg, compared with 700 kg in China and a global average of 250 kg.

At such an early phase on the steel intensity curve, India’s economy will grow alongside its demand for steel. This also means that the growth in domestic production to meet demand will by dominated by primary routes consuming iron ore, as there is no significant legacy of steel construction in India from which to derive scrap for secondary processing.

At present, the Indian steel industry is particularly emissions intensive. This is due to a combination of factors, such as the use of rotary kilns with coal gasification, the low quality of domestic coal and iron ore, and a significant number of small or aged production sites.

As India rapidly expands, newer equipment and consolidation will bring improved rates of efficiency, but only a systemic shift away from coal can avoid lock-in to significant releases of carbon dioxide and methane.

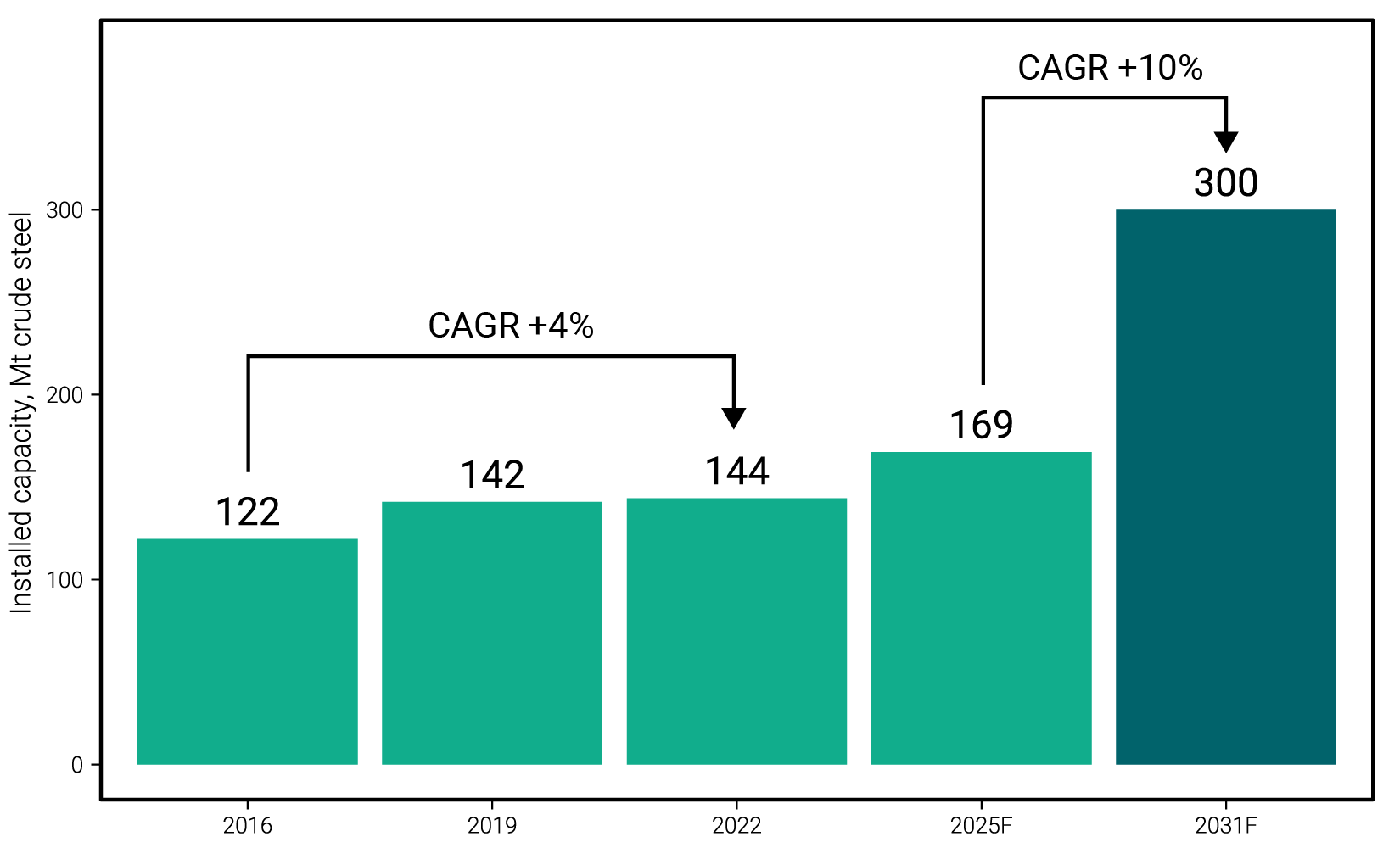

Figure 1. Steel production capacity forecast for India

Fast expanding steel capacity

With the goal of doubling annual steel production capacity to 300 Mt by 2031, the Indian Government has set the conditions for rapid expansion and companies are getting in on the act.

Five companies plan a total 114 Mt of new steel capacity. Tata Steel plans to double its Indian capacity to 40 Mt per year. JSW Steel is eying 50 Mt, up from 27 Mt, while the Steel Authority of India (SAIL) aims for 35 Mt from 20 Mt. Jindal Steel and Power (JSPL) – a relatively small producer – is attempting an astonishing five-fold increase to 50 Mt.

And those are just the domestic players, ArcelorMittal and Nippon Steel aim to triple the capacity of their joint venture AM/NS to 30 Mt, and POSCO is breaking into the Indian market through a US$ 5 billion partnership with Adani for a new plant.

Figure 2. Planned steel production capacity expansion in India from key producers

AM/NS is also planning a giant 24 Mt greenfield integrated plant in the district of Kendrapara, of which at least 12 Mt should be installed by 2030. The OECD classifies the site as being based on the blast furnace route4. Though ArcelorMittal, Nippon Steel, and AM/NS have yet to publish any information to confirm this, it is likely that the site will be majority, if not completely, blast furnace based.

Reverting to traditional coal-based methods

Based on these plans, most of the steel capacity growth in India entails the deployment of traditional blast furnace technology.

The blast furnace – basic oxygen furnace (BF-BOF) route accounts for about 70% of global steel production, and over 90% of primary steel production5. The process needs metallurgical coal. The coal is refined into coke and fed into the furnace where it provides: 1. heat energy to raise temperature, 2. carbon for chemical reduction, and 3. physical properties that support other materials while allowing off-gasses to permeate through and exit the furnace.

The only present alternative that avoids the use of coal is direct reduction (DR) based on natural gas or hydrogen (HDR). However, blast furnaces are the technology of choice in India as they are built larger, which, in the context of accelerated deployment, is seen as preferable for scaling up efficiently. Blast furnaces are also better at handling lower-grade iron ore, which is of greater relevance in a country like India with low-quality ore deposits.

Nonetheless, a wider consideration of factors suggests that the blast furnace represents a sub-optimal technology pathway for steel companies to follow. Moreover, because new blast furnaces are intended for 40 years of near-continuous operation – 25 years from commissioning and 15 years following the first reline – the risk of carbon lock-in is undeniable.

According to a 2021 study by think tank E3G and the US Department of Energy’s Pacific Northwest National Laboratory6, nearly all blast furnaces without carbon capture, utilisation and storage (CCUS) would need to be phased out by 2045 to align with a 1.5°C scenario, and this excludes supply chain emissions.

More than Scope 1 and 2 emissions

While steel companies develop their targets and transition plans based on Scope 1 and 2 emissions7 alone, comparing technologies on a level playing field also requires consideration of supply chain carbon dioxide and fugitive methane. Adapted from an IEA report for the G7 on net zero industry8, Figure 3 compares the emission intensities of key steelmaking routes with upstream emissions included.

Figure 3. Emissions intensity, including supply chain emissions, by steelmaking route

Beyond the IEA report, we include indirect upstream methane, which derives from the energy used in the production of imported electricity and hydrogen, and is therefore necessary when distinguishing blue hydrogen from green hydrogen. We also incorporate a 20 year global warming potential (GWP) for methane. Over a 100 year time period, methane is 30 times more powerful at warming the planet than CO2, but over a 20 year period it has a GWP of 83. From the perspective of avoiding a 1.5C overshoot, this is a more appropriate measure.

With this boundary it not possible for steel companies to achieve near-zero, or “green”, steel production with blast furnaces, with or without CCUS. This is because the metallurgical coal they consume is linked to fugitive releases of methane at the coal mine. Even if progress on CCUS had not proven to be slow, which it has9, capturing emissions at the steel plant does not affect emissions at the coal mine.

This also further underlines the limitations of injecting blast furnaces with hydrogen. Hydrogen injection can reduce the requirement for coke, and therefore coal, but coke is critical for its chemical and physical properties, which sets a lower limit on its consumption for stable operating conditions.

Nippon Steel, who are leading in the development of hydrogen injection, can confirm only 10% emissions avoidance under the COURSE50 programme, and >10% under the Super-COURSE50 programme10. Higher reduction goals, of 30% and 50% respectively, have also been stated by Nippon Steel but only after combining with CCUS11. Besides, full implementation for COURSE50 is not expected until the 2030s, and for Super-COURSE50 as late as 2050.

Steel companies need to start factoring in supply chain emissions when designing their transition plans, which ultimately boil down to steelmaking routes. But there are also implications for “green steel” certification and net-zero status, with certifiers such as ResponsibleSteel, the Science Based Targets initiative (SBTi), and the Climate Bonds Initiative, all including supply chain methane in some form for the steel sector.

Accounting for the dynamics of transition costs

About 70% of the cost of steel production is linked to the cost of energy and raw materials. The key to understanding this as a transition risk is by examining the relative cost dynamics of three resources: iron ore, metallurgical coal, and hydrogen.

According to research by the Institute for Energy Economics and Financial Analysis (IEEFA)12, there is mounting evidence that the future supply of metallurgical, or “coking”, coal will be more limited than previously thought.

It is no surprise that India is very concerned about this. India imports 85% of its coking coal, mostly from Australia. Coking coal can account for 40% of BF-BOF steel operating expenditure, so when prices spiked by 70% in late 2022, this would have wiped out quarterly profits in a sector already used to thin margins.

The situation is likely to get worse. As mining companies BHP, Teck Resources, and South32 move their attention away from metallurgical coal13, HSBC stated in December 2022 that it would no longer finance the development of new metallurgical coal mines14. Steel producers in India may soon need to invest in their own mines in the hope of a viable business model.

In contrast to this, the outlook for hydrogen is one of cost reductions and increasing certainty. In a June 2022 report published by Indian policy think-tank NITI Aayog and the Rocky Mountain Institute (RMI)15, large-scale deployment of green hydrogen could save India US$ 246-348 bn in energy imports, reduce resource price volatility, and provide a foreign exchange advantage.

Low-cost solar is already well established in India, giving it a clear advantage for producing cheap green hydrogen. Furthermore, the Indian government is now planning to scale up green hydrogen production to 25Mt by 2047. With the cost of renewable electricity and electrolyzer equipment set to decline, we see HDR-EAF steel production in India potentially becoming cost-competitive with BF-BOF steel in the 2030’s.

According to another IEEFA report16, the cost and availability of high-quality Iron ore for direct reduction is uncertain. DR-grade iron ore is a scarce resource, representing just 3% of seaborne iron ore trade. Options for increasing the iron (Fe) content of ores by expanding magnate mining and beneficiation are limited, in-part due to long lead times for mine project proposals.

The key to overcoming concerns over DR-grade iron ore supply is to modify the steelmaking process. Mining companies such as Rio Tinto, Vale, Fortescue, and BHP are collaborating with steel companies to get around the requirement direct reduction has for high-grade iron ore pellets.

BlueScope Steel17 and ArcelorMittal18 are enabling DR plants to function on low-grade ore by adding a special melting step and then converting to steel in a basic oxygen furnace (BOF). ThyssenKrupp is planning to replace blast furnaces with this approach from 202519. In addition, POSCO and equipment supplier Metso have developed full-scale demonstrations, HyREX20 and Circored21 respectively, that achieve direct reduction using BF-grade iron ore fines.

So a critical distinction to be made here is that, while following the DR technology pathway has options for alleviating raw material supply risks, the blast furnace route is certain to lock-in dependence on coking coal for decades to come.

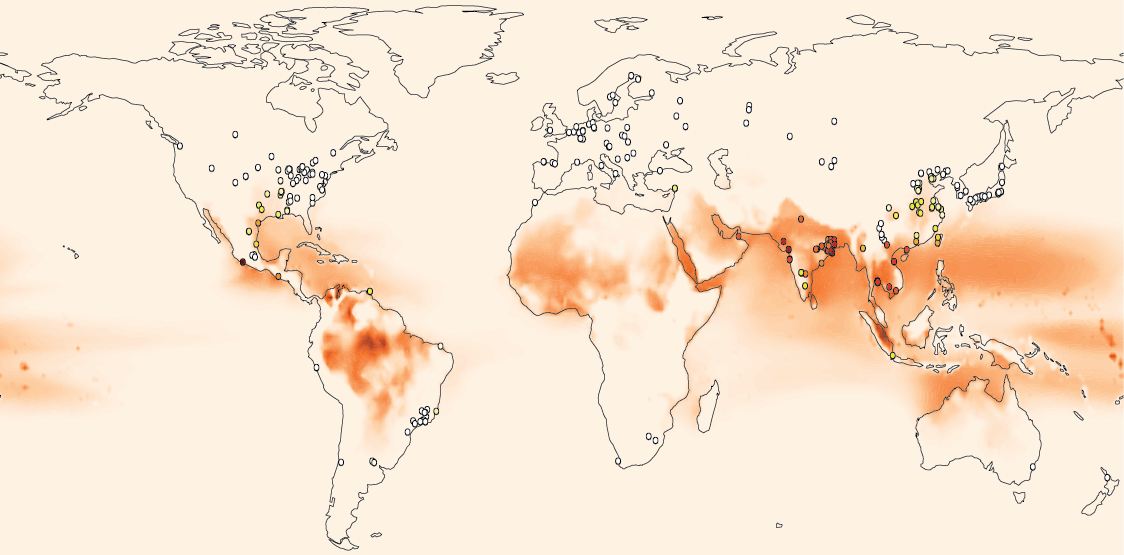

Another inconvenient truth: physical risk

Our analysis has uncovered significant disparity in exposure to physical risks among the world’s major steel producing companies. This results from the wide distribution of steel producing assets coupled with the geographical sensitivity inherent in heat and water stressors. However, there are also technological factors.

Figure 5. Distribution of heat stress and production assets of top 30 steel companies

Iron ore reduction in a blast furnace occurs at temperatures in excess of 1,500°C, whereas a direct reduction plant reaches temperatures of around half this because it is not necessary to smelt the raw material.

Blast furnace operation, therefore, has a greater requirement for cooling water than has direct reduction. Moreover, where hydrogen is used as the reducing agent, as with HDR, emissions are not of carbon dioxide but of water vapour, which can be collected and recycled back into the process.

Blast furnaces also come with more ancillary plant, such as the BOF and coke ovens, that combine to require more land area and a larger concentrated workforce per tonne of steel. In contrast, direct reduction plants are modular, do not require co-location with the EAF, and can viably be redeployed elsewhere if necessary.

Furthermore, blast furnaces must be run continuously to be profitable. Disruptions in operation hurt energy efficiency and require manpower to manage a curtailed operating regime and avoid a full shutdown. If this happens, the furnace interior hardens into a solid mass of iron, so that restoring production requires the furnace to be dismantled and replaced with a new one.

These factors suggest that the blast furnace route is significantly more exposed to physical risks. This is especially relevant for India, where heat and water stress risks are higher than in almost any other steel producing country.

Footnotes

- WorldSteel, 2023. Short Range Outlook April 2023

- United Nations, 2023. India poised to become world’s most populous nation

- Economist, 2022. India will become the world’s most populous country in 2023

- OECD, 2022. Latest Developments in Steelmaking Capacity, December 2022

- WorldSteel, 2023. Steel Statistical Yearbook 2022. Analysis from Carbon Transition Analytics.

- E3G and PNNL, 2021. Decarbonizing the Steel Sector in Paris Compatible Pathways

- Scope 1 emissions are direct emissions from owned assets. Scope 2 emissions are associated with purchased utilities such as electricity.

- IEA, 2022. Achieving Net Zero Heavy Industry Sectors in G7 Members

- IEA, 2023. Energy Technology Perspectives. p189

- ChallengeZero. Development of CO2 emission reduction technology using hydrogen in blast furnace steelmaking

- Nippon Steel. Promotion of innovative technology development. Accessed 01 June 2023.

- IEEFA, 2023. ArcelorMittal: Green steel for Europe, blast furnaces for India

- IEEFA, 2023. HSBC joins major miners in turning away from further metallurgical coal mine development

- HSBC, 2022. HSBC Thermal Coal Phase-Out Policy, December 2022.

- NITI Aayog and RMI, 2022. Harnessing Green Hydrogen: Opportunities for Deep Decarbonisation in India

- IEEFA, 2022. Iron Ore Quality a Potential Headwind to Green Steelmaking.

- BlueScope, 2021. BlueScope and Rio Tinto sign MOU for low-emissions steelmaking at PKSW.

- ArcelorMittal, 2021. Air Liquide and ArcelorMittal join forces to accelerate the decarbonisation of steel production in the Dunkirk industrial basin

- ThyssenKrupp, 2020. Electrical hot metal from blast furnace 2.0: thyssenkrupp presents Federal Economics Minister Altmaier and State Premier Laschet innovative concept for green transformation of Duisburg steel mill.

- POSCO, 2022. Great Conversion to Low-carbon Eco-friendly Steelmaking Process: HyREX

- Metso, 2021. Decarbonizing steel production: Metso Outotec launches next generation of the 100% hydrogen-based Circored process for fine ore reduction respectively, that achieve direct reduction using BF-grade iron ore fines